BUSINESSES CONTINUE BUILDING BUFFER STOCKS IN ANTICIPATION OF FURTHER DISRUPTION AS SUPPLY SHORTAGES PERSIST: GEP GLOBAL SUPPLY CHAIN VOLATILITY INDEX

- Manufacturers' reports of supply shortages among their highest since late 2022, signaling supply-chain bottlenecks will continue into at least the third quarter

- Businesses continued building buffer inventories, driving another month of strong demand for raw materials, commodities and intermediate goods

- Demand stayed strong in North America and Asia, but European manufacturers retrenched in June

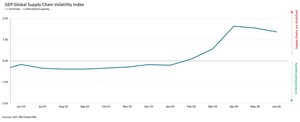

CLARK, N.J., July 13, 2026 /PRNewswire/ -- GEP Global Supply Chain Volatility Index — a leading indicator of supply-chain conditions based on a monthly survey of 27,000 businesses — showed global supply chain pressures remained elevated in June despite falling oil prices and lower transportation costs, reflecting uncertainty surrounding the US-Iran ceasefire.

Reports from manufacturers of backlogs rising due to shortages of critical inputs were their highest since late 2022. The data suggests supply-chain bottlenecks are likely to persist into at least the third quarter as businesses wait for materials needed to complete customer orders.

To guard against further disruption, manufacturers continued building buffer inventories in June. Reports of safety stockpiling increased again and remained at their highest level since January 2023.

Demand for raw materials, commodities and intermediate goods remained strong across North America and Asia, reinforcing expectations that supply-chain activity will stay elevated in the coming months as inventories are replenished and existing orders are fulfilled. In contrast, input demand weakened across Europe.

"The rise in stockpiling and persistent order backlogs point to one clear conclusion: businesses still don't trust the global trading environment to remain stable," said John Piatek, vice president, consulting, GEP. "Despite lower oil prices and easing transportation costs, companies continue buying ahead because they expect further disruption. While this is encouraging for the global economy in the near term, it also shows manufacturers remain very cautious and are planning for more disruption in international trade."

Interpreting the data:

Index > 0, supply chain capacity is being stretched. The further above 0, the more stretched supply chains are.

Index < 0, supply chain capacity is being underutilized. The further below 0, the more underutilized supply chains are.

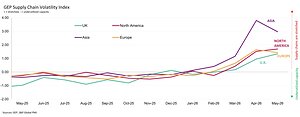

JUNE 2026 REGIONAL KEY FINDINGS

- ASIA: Index fell to 1.95, from 2.96, its lowest level since March. Easing transport cost inflation was a key factor behind the index decline in June.

- NORTH AMERICA: Index fell to 1.17, from 1.69, also a three-month low. North American goods producers raised their purchasing activity sharply, however, in response to item shortages and rising backlogs.

- EUROPE: Index fell to 1.13, from 1.43. Factories in Europe reduced buying volumes to the greatest degree since the outbreak of the Middle East war, although data shows strong inventory growth.

- U.K.: Index fell to 1.05, from 1.34, its lowest level since April as U.K. manufacturers retrench.

JUNE 2026 KEY FINDINGS

- DEMAND: Purchasing of raw materials, commodities and intermediate goods required by manufacturers to produce remained strong in June. North America and Asia were the principal drivers of this strength as European factories retrenched. In the US, input buying rose at its fastest rate since April 2022. Japan, China and Vietnam were the Asian markets which saw accelerated purchasing expansions.

- INVENTORIES: Reports of stockpiled materials rising due to price or supply concerns rose once again in June and were the highest since January 2023, signalling a sustained uplift since the Middle East war began. The data suggest that procurement managers around the globe are holding surpluses to protect against shortages and inflation.

- MATERIAL SHORTAGES: The items in short supply indicator decreased in June, indicating some dissipation of shortages across the globe. That said, supply issues remained high by historical standards, with the underlying index recording well above its long-term average. Notably, backlogs of work have risen sharply due to inadequate item availability.

- LABOR SHORTAGES: Manufacturing workforces are not inhibiting capacity, as reports of backlogs rising due to labor shortages were aligned with historically average levels.

- TRANSPORTATION: With June seeing a sharp decline in global oil prices, the transportation cost indicator subsequently fell. However, excluding April and May, transportation costs were their greatest since June 2022 and still high by historical standards.

For more information, visit www.gep.com/volatility.

Note: Full historical data dating back to January 2005 is available for subscription. Please contact [email protected].

The next release of the GEP Global Supply Chain Volatility Index will be 8 a.m. ET, Aug. 12, 2026.

About the GEP Global Supply Chain Volatility Index

The GEP Global Supply Chain Volatility Index is produced by S&P Global and GEP. It is derived from S&P Global's PMI® surveys, sent to companies in over 40 countries, totaling around 27,000 companies. The headline figure is a weighted sum of six sub-indices derived from PMI data, PMI Comments Trackers and PMI Commodity Price & Supply Indicators compiled by S&P Global.

- A value above 0 indicates that supply chain capacity is being stretched and supply chain volatility is increasing. The further above 0, the greater the extent to which capacity is being stretched.

- A value below 0 indicates that supply chain capacity is being underutilized, reducing supply chain volatility. The further below 0, the greater the extent to which capacity is being underutilized.

A Supply Chain Volatility Index is also published at a regional level for Europe, Asia, North America and the U.K. For more information about the methodology, click here.

About GEP

GEP® delivers AI-native procurement and supply chain solutions that help global enterprises become more agile and resilient, operate more efficiently and effectively, gain competitive advantage, boost profitability and increase shareholder value. Fresh thinking, innovative products, unrivaled domain expertise, smart, passionate people — this is how GEP SOFTWARE™, GEP STRATEGY™ and GEP MANAGED SERVICES™ together deliver procurement and supply chain solutions of unprecedented scale, power and effectiveness. Our customers are the world's best companies, including more than 1,000 Fortune 500 and Global 2000 industry leaders who rely on GEP to meet ambitious strategic, financial and operational goals. A leader in multiple Gartner Magic Quadrants, GEP's cloud-native software and digital business platforms consistently win awards and recognition from industry analysts, research firms and media outlets, including Gartner, Forrester, IDC, ISG, and Spend Matters. GEP is also regularly ranked a top procurement and supply chain consulting and strategy firm, and a leading managed services provider by ALM, Everest Group, NelsonHall, IDC, ISG and HFS, among others. Headquartered in Clark, New Jersey, GEP has offices and operations centers across Europe, Asia, Africa and the Americas. To learn more, visit www.gep.com.

Media Contacts

Derek Creevey |

Joe Hayes |

S&P Global Market Intelligence |

Director, Public Relations |

Senior Principal Economist |

Corporate Communications |

GEP |

S&P Global Market Intelligence |

Email: [email protected] |

Phone: +1 646-276-4579 |

Phone: +44-1344-328-099 |

|

Email: [email protected] |

Email: [email protected] |

SOURCE GEP

Share this article