Li-ion Battery Cathode and Anode Ten-Year Material Outlook, by IDTechEx

BOSTON, Dec. 2, 2025 /PRNewswire/ -- An analysis of the materials adopted in li-ion batteries quantifies the change of cathode and anode materials used over the coming decade, with the increase of ultra-high nickel cathodes and high silicon anodes. The full assessment is provided in the new IDTechEx report Li-ion Battery Market 2026-2036: Technologies, Players, Applications, Outlooks and Forecasts.

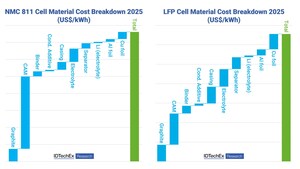

Li-ion battery cathode outlook

Cathodes play a dominant role in defining cell energy density, and also make up a significant proportion of cell costs, due to the use of high-cost metals such as cobalt, nickel and lithium. Standard cathode choices are lithium nickel manganese cobalt oxides (NMC) and lithium iron phosphate (LFP). NMC provides high energy density at a higher cost, while LFP can provide lower cost per kWh when space is not at a premium. LFP has become increasingly dominant in China, especially for stationary energy storage, though it has also seen increasing use in electric vehicles, Meanwhile, NMC is widely used in Europe and North America, and has seen trends towards higher nickel content, as a result of high cobalt prices.

Ultra-high-nickel NMC/NCA/NMCA have started to be introduced and will constitute a more important portion of the market, primarily within premium and long-range battery electric cars from the late 2020s/early 2030s. Similarly, LMFP cathodes will start to see adoption from the second half of the 2020's, offering a high energy density option to LFP with a similar cost profile.

IDTechEx Technology Analyst Daniel Parr concludes, "Demand for LFP and LMFP is forecast to reach 2683 GWh by 2036, while demand for high and ultra-high nickel NMC/NCA/NMCA will reach 2207 GWh."

Li-ion Battery Anode Materials

For battery anodes, by GWh, the majority of the Li-ion battery market will continue to be graphite based (where silicon anode material is incorporated at less than 10wt%). Parr reports, "While IDTechEx are relatively positive on the outlook for silicon-based anode materials it will take time for more advanced materials that allow the addition of silicon material at 10-50 wt% of the anode (mid-silicon) or at >50 wt% (high-silicon/silicon dominant) to enter the market."

Silicon anodes can enable Li-ion energy densities above 1000 Wh/l and 400 Wh/kg, while rate capability and charging times can also be improved. However, achieving long-term cycle stability has been a significant challenge due to the expansion of silicon under lithiation.

Some low volume and early adoption of advanced silicon anode solutions have been seen in fitness wearables, smartphones, drones, and electric motorcycles.

Overall, IDTechEx report that the Li-ion battery cell market is forecast to grow to US$325 billion by 2036 at a CAGR of 7.0%.

For the full analysis from IDTechEx, covering ten-year battery demand and breaking down the market by both application and lithium-ion battery chemistry, including NMC, LFP, graphite-anode, silicon-anode and more, see IDTechEx's recent report: Li-ion Battery Market 2026-2036: Technologies, Players, Applications, Outlooks and Forecasts.

About IDTechEx

IDTechEx provides trusted independent research on emerging technologies and their markets. Since 1999, we have been helping our clients to understand new technologies, their supply chains, market requirements, opportunities and forecasts. For more information, contact [email protected] or visit www.IDTechEx.com.

Media Contact:

Charlotte Martin

01223812300

[email protected]

SOURCE IDTechEx

Share this article